Table of Content

Single-family home construction runs about $150 per square foot and new homes of 2,000 square feet run nearly $307,000. Considering the incredible cost difference, it doesn’t make good dollars or sense to buy a used mobile home. Moreover buying a new manufactured home can give you the chance to customize it to your needs. Even if it is cheaper to buy a mobile home that was used before but you end up with more expense trying to make it yours by renovating it. When thinking about what to do when buying a “mobile home” or “manufactured home,” one of the first considerations is whether to purchase or lease land. Making this decision should be a high priority on your checklist before buying a manufactured home.

There are many types of loans to choose from, even if you don’t have great credit. A government agency or a private enterprise can back a mobile home mortgage. A private enterprise usually has more flexibility to determine its own risks. A bad credit score could mean you don’t get to borrow as much as you’d like.

How much income do you need to qualify for a $300 000 mortgage?

Many lenders are skeptical about manufactured homes built before 1976, meaning you may find it hard to secure financing. A manufactured home is worth your time and money because it is less costly compared to a traditional site-built home, and you may use a personal loan to finance your home. Read more about the answer to ‘should I build a house or buy a manufactured home’ here. It is feasible to improve your score and, hence, your chances of receiving better loan terms in the future. With that said, this is a lengthy process that requires consistency and financial discipline.

In the United States, manufactured homes are popular because they are less expensive than typical real estate dwellings. A USDA home loan is a competitively priced mortgage option that helps to make purchasing a home more affordable for low-income individuals living in designated rural areas. The U.S. The Department of Agriculture backs USDA loans in the same way the Department of Veterans Affairs backs VA loans for eligible individuals such as veterans and their families. Compare lenders – Not only should you compare the type of loan, but see how fees and interest rates vary among lenders. Bigger homes may not be eligible for some loans – Buying a double-wide home that costs $100,000 or more isn’t allowed in an FHA loan.

Local and National Mortgage Programs for First Time Home Buyers

Lenders use this information to calculate your credit score. The higher your score, the more likely they are to lend you money. We make every effort to provide up-to-date information, however we do not guarantee the accuracy of the information presented. Consumers should verify terms and conditions with the institution providing the products. Articles may contain some sponsored content, content about affiliated entities, or content about clients in the network. Well, my friends, the time has come to tell you what kind of blog I am.

Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions. The content created by our editorial staff is objective, factual, and not influenced by our advertisers. Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Buying or selling a home is one of the biggest financial decisions an individual will ever make.

Can you buy a mobile home with a 500 credit score?

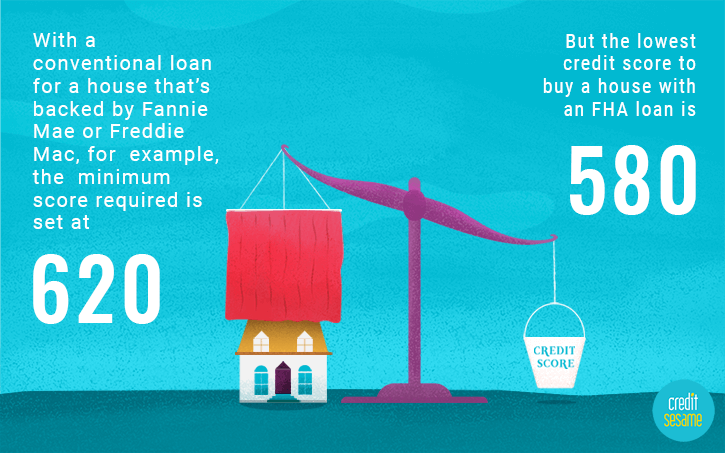

Nonconforming loans cannot be sold to Fannie or Freddie, and the minimum required credit score is up to the individuallender. Conforming loans meet certain government-set conditions that allow the lender to sell the loan to Fannie Mae or Freddie Mac. For 2023, the limit for one-unit properties is $726,200, up $79,000 from $647,200 in 2022. In high-cost areas, the limit is $1,089,300 for one-unit properties. You typically need a credit score of at least 620 to get a conforming loan.

Furthermore, unlike traditional mortgages, you will be rejected if you earn too much money. Even though mobile homes are less expensive than permanent residences, they are not cheap. To purchase a mobile home, you’ll require a substantial sum of money. Census Bureau, there are more than eight million manufactured homes in the United States, with the average cost of the purchase in 2021 being $88,000.

That said, while you are worried about other things, remember that your debt-to-income ratio, just like a credit score, represents your financial health. Yes, you can purchase a mobile home with a low credit score . A good score can help you get better loan terms , but it is not the only thing lenders look at when deciding whether or not to lend to potential mobile homeowners. Before offering a mortgage, lenders will be concerned about your debt to income ratio. Your chances of securing a mortgage are slim if you have an uneven debt to income ratio. Using 20-30% of your credit limit is often deemed acceptable.

Yes, it can be easier to get approved for a modular home since the loan process is shorter and the credit requirements are less stringent. There are exceptions, however, and weve included them in this list. Some home lenders do have loans for mobile homes if they are attached to the homeowners land. Others, and there are fewer of them, will lend on a mobile home even if it sits on land you lease. A mobile home loan is a loan for factory-built homes that can be placed on a piece of land.

Connect with us or submit your info below and we'll help guide you through your options. There are some other credit scoring models, but the most common one is the FICO score. The FICO scale ranges from 300 to 850; the higher your score, the better. A score of 800 or more is considered excellent, while a score of 740 to 799 is seen as good.

These banks each have their own scoring systems and loan programs vary slightly from lender to lender. Overall, these types of loans have much lower closing costs and fees than government-backed loans. USDA and VA loans are government-backed options without credit score minimums, but most lenders prefer a credit score of at least 640 and 620, respectively. To qualify for a no-down-payment mortgage through a commercial or private lender, you’ll likely need excellent credit. Improving your credit score can help you qualify for better mortgage rates. Start by getting current on any past due accounts, if applicable, and be sure to make timely payments moving forward.

Consider yourself a “tenant” if you don’t own the land because you’ll be paying a lot of rent to a landlord. The prequalification calculator will tell you how much money you can borrow, your monthly mortgage payment, and the highest monthly mortgage payment you can acquire. A lender and a company specializing in rapid rescoring can assist you in reporting the information to credit bureaus and resolve the issue in five business days, rather than months. Checking your reports is important to keep unnecessary errors from harming your score. For example, there could be incorrect accounts, incorrect payment statuses, among other common errors.

Additionally, it’s important to make sure that the mobile home you’re interested in has been well maintained and is in good condition. One solution is to get your credit score raised by submitting a request to your credit bureau. Divide the total amount of debt by the total number of payments.

How to Finance a Mobile Home

Whenever you apply for a new credit card, the creditor will run a hard credit check and that can potentially impact your score. That said, only apply for a new credit card if you really need it. Most people have problems with paying bills because they don’t budget their spending well. That said, make your monthly budget and schedule your payments to avoid penalties. So, if you want to improve your score, this is where you should concentrate your efforts. If you have a habit of forgetting to pay your bills, we recommend automating them.

No comments:

Post a Comment